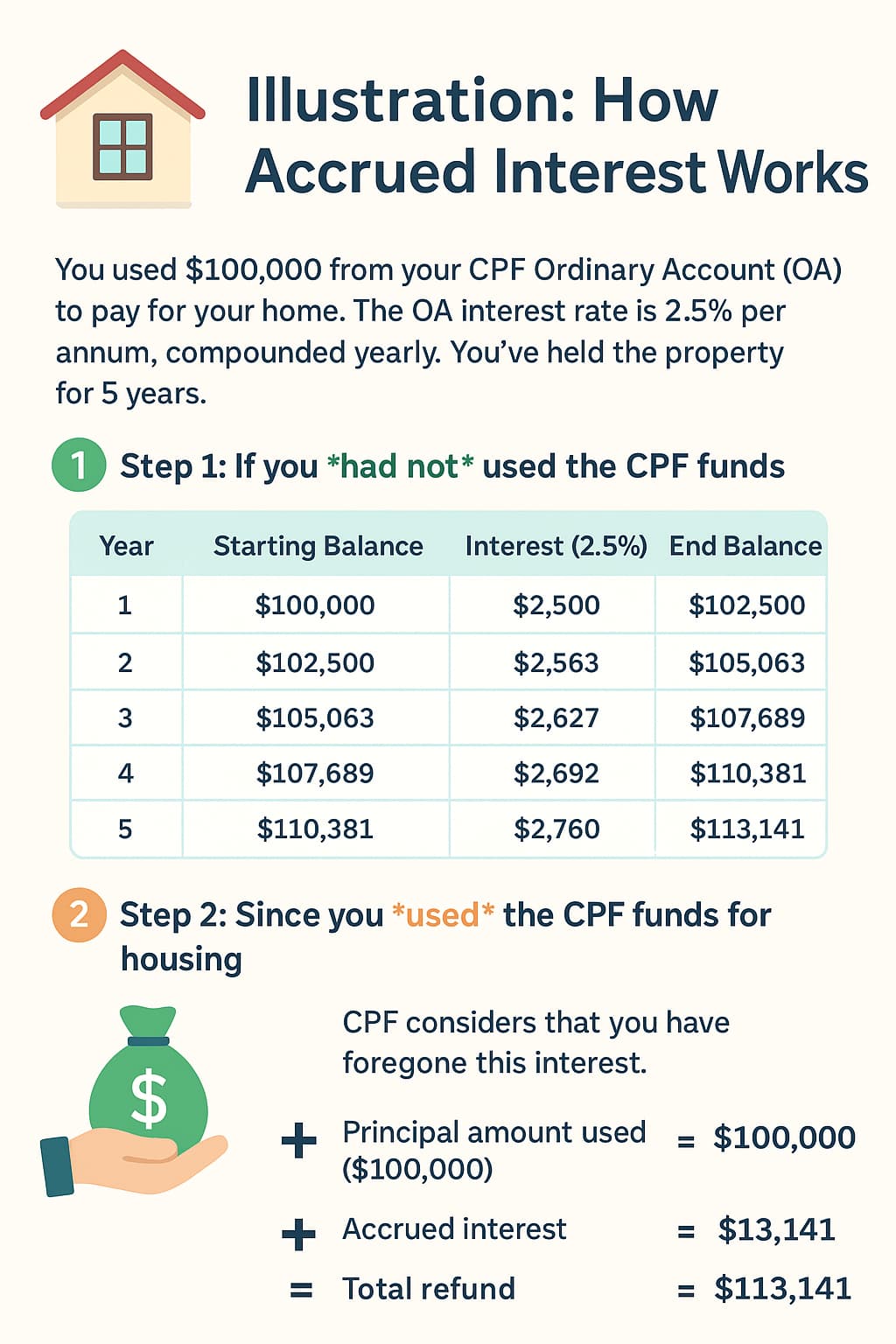

Definition: Accrued interest is the amount of interest your CPF savings would have earned had they not been withdrawn to pay for a home (e.g., downpayment and monthly instalments). This is computed based on the prevailing CPF Ordinary Account (OA) interest rate (currently 2.5% p.a. floor rate) and compounded yearly.

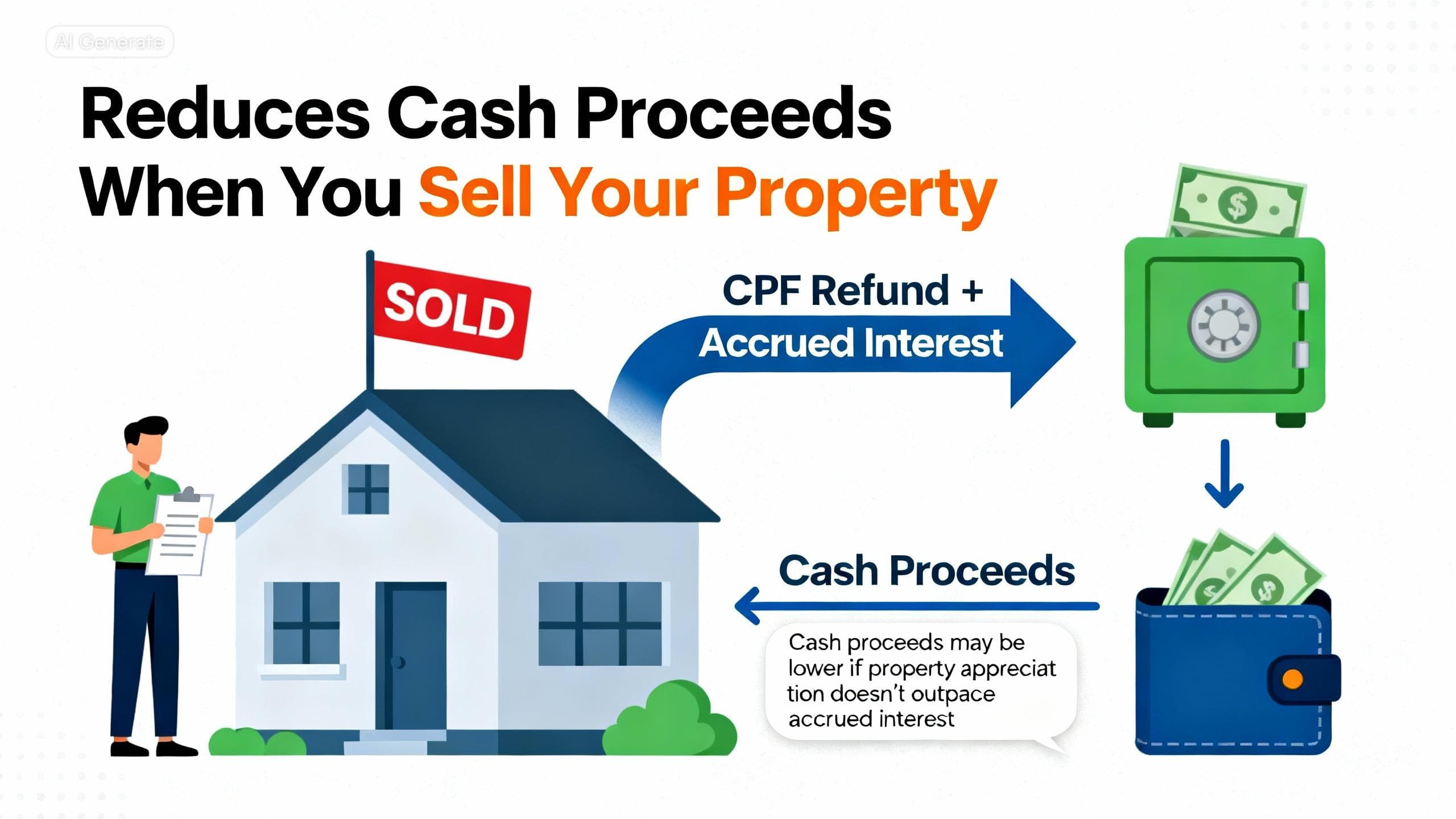

Refund Requirement: When you sell, transfer, or dispose of your property, you are required to refund the CPF principal amount withdrawn plus the accrued interest back into your CPF accounts. This is to restore your retirement savings.

Purpose: The refund ensures that your retirement fund grows steadily. The funds returned will then be used to meet your Retirement Account (RA) sum, which provides lifelong monthly payouts.

The less CPF you use, the less accrued interest will build up.

If you’ve sold a property or have spare cash, you can voluntarily refund the CPF amount you’ve used — even before selling your home.

Example: If you used $100,000 and refunded $20,000 early, you’d only accrue interest on $80,000 going forward.

When you use CPF for monthly instalments, you’re continuously adding to the principal that must later be refunded with interest.

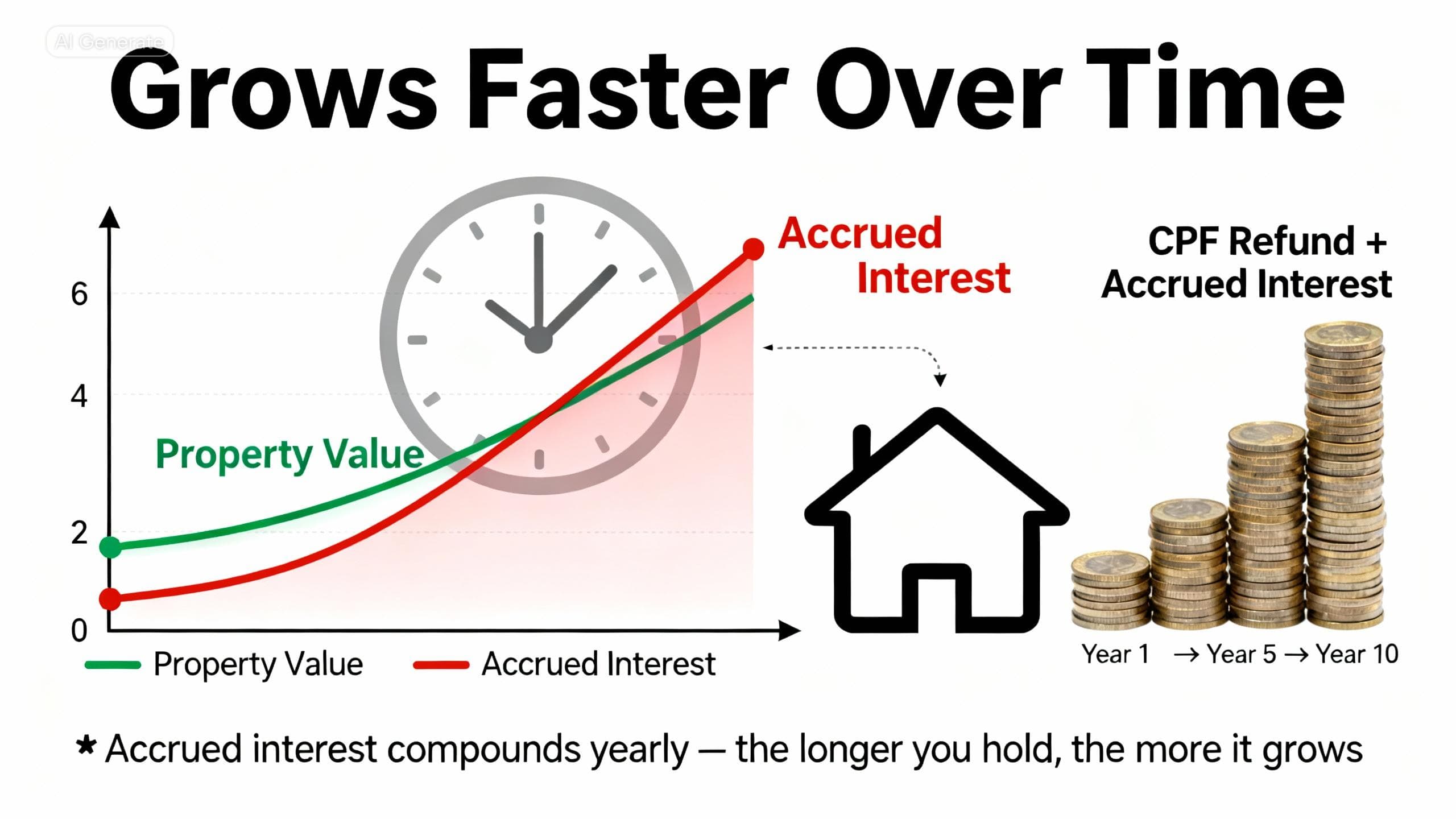

Accrued interest compounds yearly — so the longer you hold, the more it grows.

In summary, CPF accrued interest is an inescapable part of using your CPF savings for a property purchase, representing the “opportunity cost” your funds would have earned had they remained in your Ordinary Account. While it can significantly impact your net proceeds upon sale, it should not be a source of paralysis. The key lies in proactive and strategic planning.

This is where the expertise of Property Pathway becomes your greatest asset. Our seasoned agents possess an in-depth understanding of the CPF system and are specialists in crafting tailored strategies to mitigate the negative impacts of accrued interest. We don’t just facilitate a transaction; we provide a clear roadmap. By guiding you on the optimal timing, financial structuring, and seamless coordination of selling your current property and purchasing your next resale home, Property Pathway empowers you to navigate this complex landscape with ease and confidence, turning a potential financial challenge into a strategic step forward in your property journey.